Buying the Dip

Brand building in a time of recession

I can’t describe the relief I felt watching Jacinda Ardern announcing border closures and lockdowns in the early days of Covid. I had been watching Italy and then Spain get overwhelmed, and the warnings of doctors who had not slept in days – this is coming, it’s too late for us, it’s not too late for you.

Some back-of-the-napkin calculations showed that, with the exponential rate of infections and the delay between infection and symptoms, you could assume that there were something like 13 times as many infections in a country as there were reported cases. In New Zealand, we were in the low dozens of known cases, so we already had several hundred waiting to become symptomatic.

We locked down, stopped the spread, and cases kept climbing – of course they did. Every day, we watched the numbers go up, up, up, and then after about two weeks they peaked, plateaued, and then started to decline, eventually to zero. We knew the maths, we knew the visible impact of lockdowns would be delayed, but it was still tense to feel like we were taking this extreme and costly action and seeing no immediate results.

The feedback period was only a few weeks, but it was an object lesson in making decisions with no immediate effects to reap the benefits in the future.

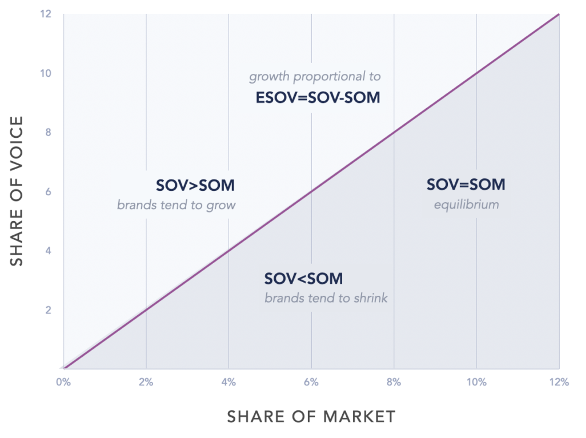

In 1990, professor John Philip Jones published an article in the HBR describing a correlation between share of voice (SOV) and share of market (SOM). Share of voice was expressed in terms of dollars spent on media – a point I’ll come back to. The relationship to share of market maps a lot to long-term brand equity. The thinking about the correlation led to a general rule of thumb for the impacts of advertising spend on market share, and thus (relative) profits.

“Relative” is a key word here. This image from the School of Marketing illustrates the theory involved.

The idea is that, all other things being equal, if all brands spend proportionately to their share of market, those shares will all stay the same. For example, if a Brand X has 30% of the market and the total category spend on advertising is $10 million, then if Brand X makes up $3 million of that category spend, its share of market will keep steady.

What happens if Brand X spends $5 million while everyone else keeps their budgets the same? Well, now the category spend is $12 million and Brand X’s share of it is about 41%. That’s 11 points higher than its share of market, and that difference is called its excess share of voice (eSOV).

What’s the impact of this eSOV? According to the theory, the rule of thumb is that for every 10 points of eSOV, you can expect market share to increase by 0.5% in a year.

That sounds frustratingly small, but when you’re dealing with very high volumes of revenue, 0.5% of the total category (customer) spend is nothing to be sneezed at. And of course, as is common with these kinds of theories, it provided a very reassuring framework for budgeting and had the added advantage of being quantitatively measurable. That is, compared to many other factors understood to contribute to marketing success, it felt much less subjective to talk about budget allocations than, say, how inspiring a brand purpose was.

Now, there are plenty of criticisms of this theory of eSOV.

For one, those five words above – “all other things being equal” – are doing a lot of work. Because there are many many other things to be unequal. To list a few…

The eight factors of product quality – features, performance, reliability, durability, conformance, serviceability, aesthetics and perceived quality.

The effects of channels and channel partners – selling online, using CRMs, placements in retail stores – and the effects of sales teams and word of mouth.

Strategic marketing and brand choices – segmentation/targeting, positioning, points of difference, points of parity, user/usage imagery, etc.

Executional factors like creative quality, brand consistency, etc.

Non-budget-related media factors like channels, formats, timing, targeting.

Creative and brand agencies in particular balk at the notion that the impact of advertising can be boiled down to outspending the other guys. And justifiably so. Their work is an amplifier (or attenuator) of the impact of that budget. (Media agencies, on the other hand, big fans.)

But, of course, all of the competitors also have creative and brand agencies also doing their best to amplify (and not attenuate) the impact of those competitors’ budgets.

Secondly, SOV was a lot easier to talk about in 1990. The number of advertising channels available were very limited, so share of voice in those channels was very measurable and also zero-sum – if one brand got more space, another brand got less. Today’s media environment is exponentially more fragmented, much more difficult to compare spends, and much more difficult to translate relative spend into actual relative share of voice.

That is, can we really compare $50k spent on sponsoring a popular two-million-fan Twitch streamer with $100k spent on evening-drive radio spots? Does one really have twice the voice of the other? In theory (saying that a lot in this post), there is an efficient-market element at work here. That is, over time, the relative return of $50k on one media type should become about half the value of $100k on another media type. Because underpriced media will get gobbled up by the planning experts and those media will lift their prices to a market equilibrium. And overpriced media will lose sales to more efficient channels until they drop their prices. Yay, theory.

With all of the above said, let’s imagine there is still something to the idea of eSOV. It’s intuitively true that if you’re the only brand spending on advertising while your competitors spend none, you’ll gain market share. And it’s intuitively true that if all of your competitors advertise and you spend nothing, you’ll lose market share to them. In the long run. And where we sit is somewhere between those extremes of 0% and 100% of share of voice.

If you hadn’t noticed, the economy isn’t doing so well. And when belts get tightened, marketing budgets are often first on the chopping block, to mix some metaphors.

And that’s completely understandable. Unlike almost any other expenditure in a business, marketing dollars disappear out the window without immediate effect. More to the point, cutting that budget lacks the immediate negative effects of cutting staff, halting the purchase of inputs, failing to pay suppliers or rent on office space, etc. If sales are down, revenue is down, and balancing the books means dropping the other side of the cashflow statement.

Of the remaining marketing dollars, what kind of spend gets prioritised? Well, the faster the return on the spend, the more appealing it is financially. Spending on sales promotions can see a return within the same financial reporting cycle, while the effects of brand building are long-term and less dramatic. Again, more to the point, cutting spend on brand building has probably zero effect within that reporting cycle.

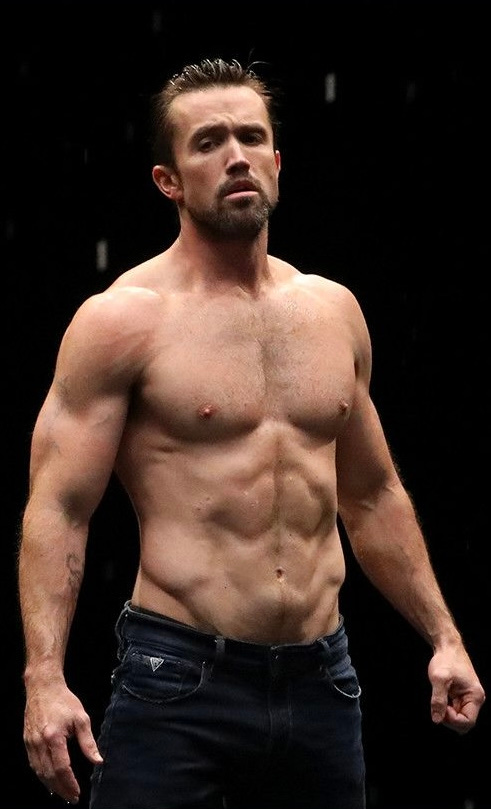

Like muscle strength, flexibility, or cardio fitness, brand equity builds up with effort over time. And also like those things, brand equity fades very gradually over time. If Rob McElhenney stops working out for a few weeks, he still looks like this:

His interviews about how long and hard it was for him to get looking like this are hilarious. But his investment will keep him looking like that for quite a while after he stops actively maintaining it. It’ll even make it easier for him to stay there than it was for him to get there – all them pecs and lats and whatnot are burning calories just by existing. Insane transformation. How good was the ballet episode? Brilliant show.

So a business can coast for some time on the effects of past brand building. I think it was Mark Ritson who likened it to an airplane cutting its engines. The momentum keeps it airborne for a while before it starts to plummet. His point was also that, once the plane starts plummeting, it takes more fuel to get it back to where it was than it would have taken to maintaining cruise altitude.

I’m full of metaphors today, aren’t I.

So let’s put these things together.

The theory of excess share of voice is that relative spend, not absolute spend, determines the market-share effect of advertising.

In a recession, businesses cut spending and brand building is the logical expenditure to cut with no consequences within the critical short-term horizon.

The effects of brand building are long-term, gradual and persistent.

According to the eSOV theory, if every competitor in a category halves their advertising spend, none of them will suffer for it. (Arguably the category as a whole will suffer, but in the recession, categories suffer as a whole anyway.) So of whatever remaining total customer spend there is in the category, if the relative shares of voice are stable, the relative shares of (the temporarily smaller) market will be stable.

One more analogy.

When Covid hit, the share market dropped. There are all kinds of reasons for that, but they all manifest as: share owners were selling, and accepting lower and lower prices for their shares. This price drop was reflected in the falling reported value of long-horizon retirement funds, like Kiwisaver growth funds. I’m aware of people who saw this happening and freaked out, switching their Kiwisaver savings from growth funds to conservative funds. There’s no need here to go into the foolishness of that.

At the same time as people were selling shares for lower and lower prices, some people were buying those shares for lower and lower prices. With the same logic, while Kiwisaver growth funds were dropping, some people pumped extra money into those Kiwisaver funds.

Why? Because in a long enough timeline1, the future value of those shares wasn’t changing as much as the prices were. In essence, they were going on sale. You could buy more for the same amount of money.

I was tempted to say “clever people” rather than “some people”, but there was another requirement besides cleverness for making that move: having cash to spare.

The analogy should be clear, but I’ll spell it out anyway.

If…

eSOV is the path to long-term brand equity.

Competitors are reducing their advertising spends.

So you can achieve more eSOV per dollar spent.

And the value of future brand equity is unchanged by today’s economy.

And so future brand equity is basically on sale.

In terms of future brand equity and its impact on share of market, the same advertising spend yields greater returns if your competitors reduce their spend. Even more so if you increase your spend. More bang for your buck.

Even better, if the economy overall is cutting on ad spending, media channels are likely to drop their prices because of the lower demand. Not only does the same spend go further in relative share of voice, it goes further in absolute reach and frequency.

Sounds great, but – like with buying the dip in share investing – you’ve got to have the bucks to do it. And many businesses are unlikely to have that cash for the same reasons that many investors are unlikely to.

Firstly, why would they be sitting on cash when they could have invested it earlier?2 (Or paid out to owners.) (Or spent on a holiday.)

Secondly, the exact time that future brand equity goes on sale is the time when revenue/income becomes less certain. If you have cash reserves, they’re sensibly earmarked for the possibility of revenue shortfalls or (in the case of individual investors) job loss.

Ignore this bit if finance doesn’t interest you.

Taking advantage of that sale can be treated as an investment decision. That is, estimate the return in future cashflows of the greater market share (perhaps with the 0.5/10 rule of thumb above). Project the risks and sizes of costs that could be incurred by not having that cash on hand (or having to borrow). Discount both the cashflows, weighted by risk, back to the net present value of that option. Do the same projections and calculations for cutting your ad spend like everyone else is (including the risks that one or more competitors might not cut their spend). If the NPV of the ad-investment option is larger, it’s the smart move – assuming your assessment of the risks and returns are accurate.

And in more favourable economic times, you might consider what could be done to be prepared for next time – and do similar calculations on that “investment” of having cash available, with its return being weighted against the probability of the next recession. You’d want to update those estimates each year as the probability of recessions and expected distance in the future changes. As probabilities increase and timeframes get shorter, the NPV will increase and a cash reserve that made no sense the previous year might suddenly become a good idea.

You can uncover your ears now.

These aren’t new thoughts. I just went looking for a particular Ritson quote and found this very good article from two years ago, which covers some of the above points and adds a few other great tips for marketing in a recession.

Psychologically, when things are uncertain, it’s not easy to put the foot down on the gas pedal and nothing happens immediately. Like with the Covid lockdowns, the feedback is delayed and there’s some nail-biting as we watch things get worse before they get better.

And every business budgeting decision is a trade-off. Just because future brand equity is on sale, doesn’t mean it’s automatically the best thing to do with company resources. For example, if cash reserves can be used to save jobs instead, there’s a very good chance that is the better move – avoiding costs of hiring and training once business picks up, the morale impact on the team, and living up to the non-financial values of the company.

But at the very least, think twice before simply cutting brand-building ad budgets when your industry overall is suffering. Business is a long game and it’s a competitive game. Business strategy is how you do things differently from competitors in the long run.

One final thought – what if everyone has the same idea? If all competitors maintain or increase their spend during a downturn, the sale on future brand equity ends and everyone is paying full price, so to speak. And suddenly the balance shifts and it might have been smarter to pull back on spending. But what if everyone has that same thought and everyone pulls back on spending? Suddenly it’s smarter to increase spending… Welcome to Game Theory, very much a story for another day.

Some people’s timelines are much longer than others.

I am aware that both financial advisers and many people managing their own investments do in fact keep some wealth liquid enough for precisely this reason.